Investment management firm T. Rowe Price (NASDAQ: TROW) fell short of the market’s revenue expectations in Q1 CY2026 as sales rose 4.6% year on year to $1.86 billion. Its non-GAAP profit of $2.52 per share was 7.4% above analysts’ consensus estimates.

Is now the time to buy T. Rowe Price? Find out by accessing our full research report, it’s free.

T. Rowe Price (TROW) Q1 CY2026 Highlights:

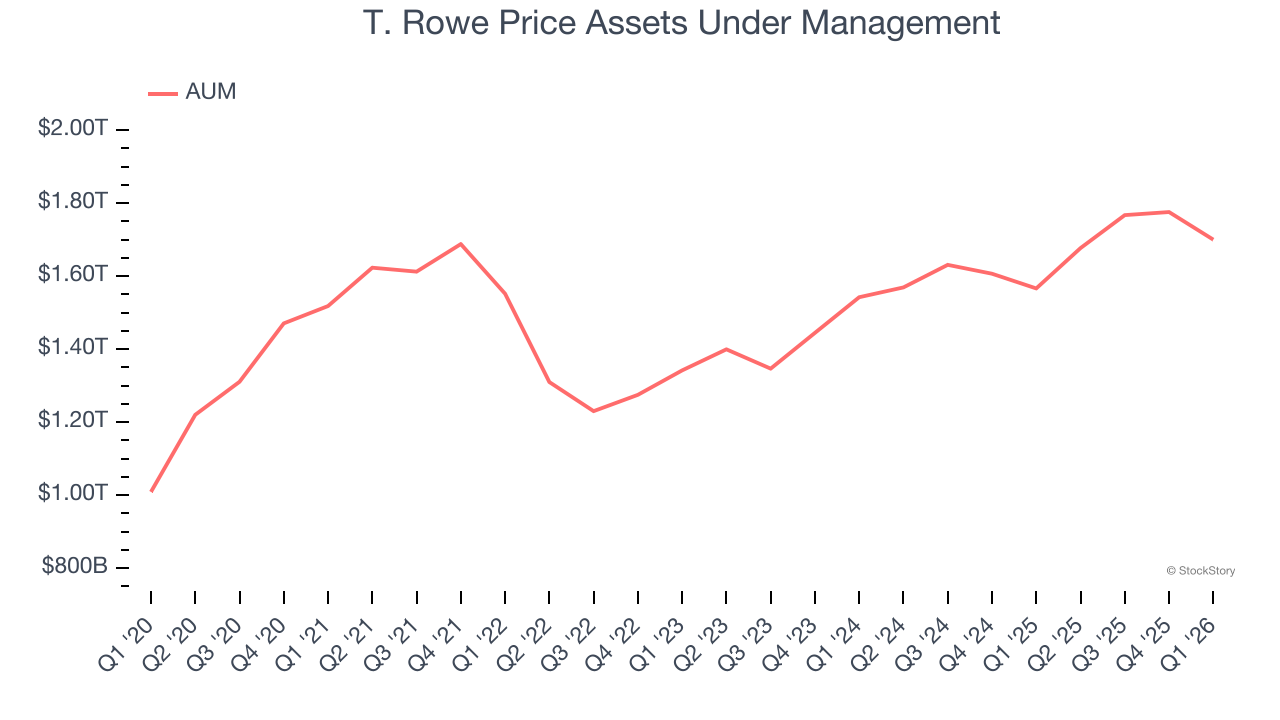

- Assets Under Management: $1.7 trillion vs analyst estimates of $1.73 trillion (8.5% year-on-year growth, 2% miss)

- Advisory and Services Fees: $1.68 billion (5.3% year-on-year growth)

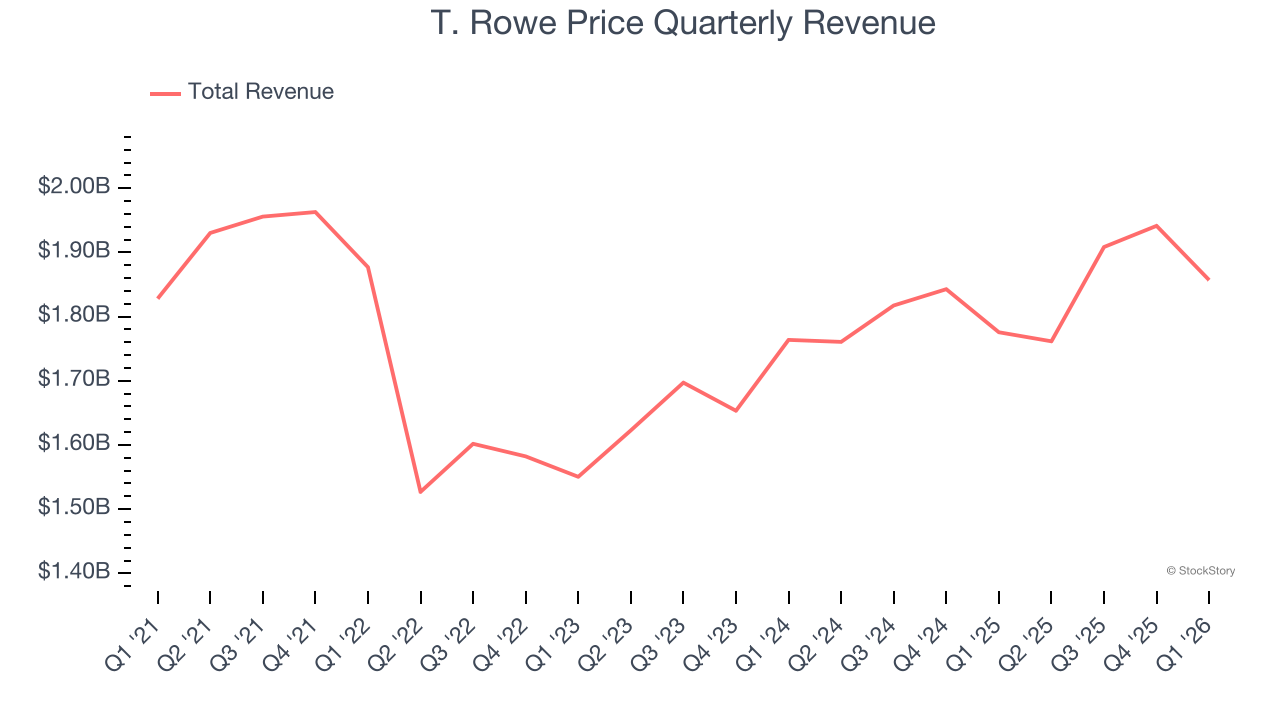

- Revenue: $1.86 billion vs analyst estimates of $1.88 billion (4.6% year-on-year growth, 1.2% miss)

- Pre-tax Profit: $632.2 million (34% margin)

- Adjusted EPS: $2.52 vs analyst estimates of $2.35 (7.4% beat)

- Market Capitalization: $21.86 billion

Company Overview

Founded in 1937 by Thomas Rowe Price Jr., who pioneered the growth stock investing approach, T. Rowe Price (NASDAQ: TROW) is an investment management firm that offers mutual funds, advisory services, and retirement planning solutions to individuals and institutions.

Revenue Growth

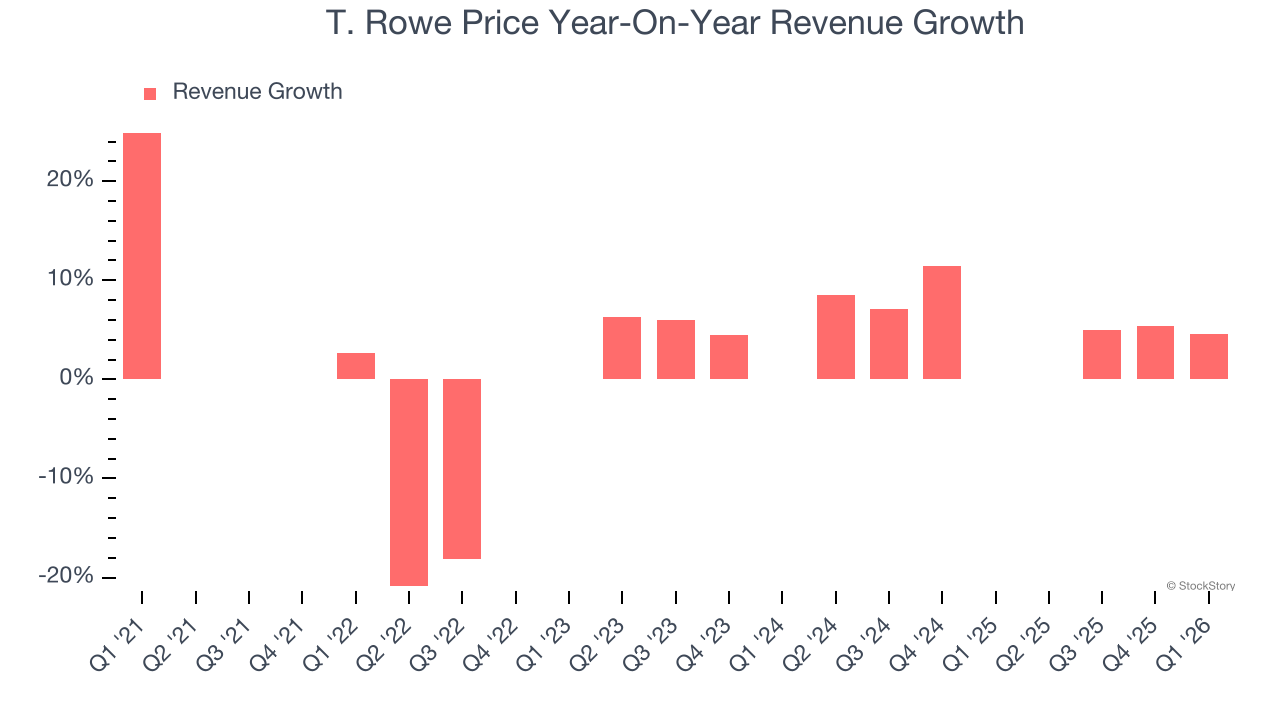

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, T. Rowe Price’s revenue grew at a sluggish 2.6% compounded annual growth rate over the last five years. This was below our standards and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. T. Rowe Price’s annualized revenue growth of 5.3% over the last two years is above its five-year trend, which is encouraging.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, T. Rowe Price’s revenue grew by 4.6% year on year to $1.86 billion, falling short of Wall Street’s estimates.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Assets Under Management (AUM)

Assets Under Management (AUM) is the total capital a firm oversees or manages on behalf of clients. Fees on this AUM, typically a small percentage, are contractually recurring and provide a high level of stability to revenue even if investment performance lags (although too much poor investment performance eventually hurts fundraising ability).

T. Rowe Price’s AUM has grown at an annual rate of 4.6% over the last five years, worse than the broader financials industry but faster than its total revenue. When analyzing T. Rowe Price’s AUM over the last two years, we can see that growth accelerated to 9.9% annually. Fundraising or short-term investment performance were net contributors for the company over this shorter period since assets grew faster than total revenue. But again, we put less weight on asset growth given how lumpy and cyclical it can be.

T. Rowe Price’s AUM punched in at $1.7 trillion this quarter, falling 2% short of analysts’ expectations. This print was 8.5% higher than the same quarter last year.

Key Takeaways from T. Rowe Price’s Q1 Results

We were impressed by how significantly T. Rowe Price blew past analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its AUM missed and its revenue fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $100.74 immediately after reporting.

So should you invest in T. Rowe Price right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).