Granite Construction currently trades at $121.57 and has been a dream stock for shareholders. It’s returned 205% since April 2021, more than tripling the S&P 500’s 61.5% gain. The company has also beaten the index over the past six months as its stock price is up 12.3%.

Is it too late to buy GVA? Find out in our full research report, it’s free.

Why Does Granite Construction Spark Debate?

Having played a role in the construction of the Hoover Dam, Granite Construction (NYSE: GVA) is a provider of infrastructure solutions for roads, bridges, and other projects.

Two Positive Attributes:

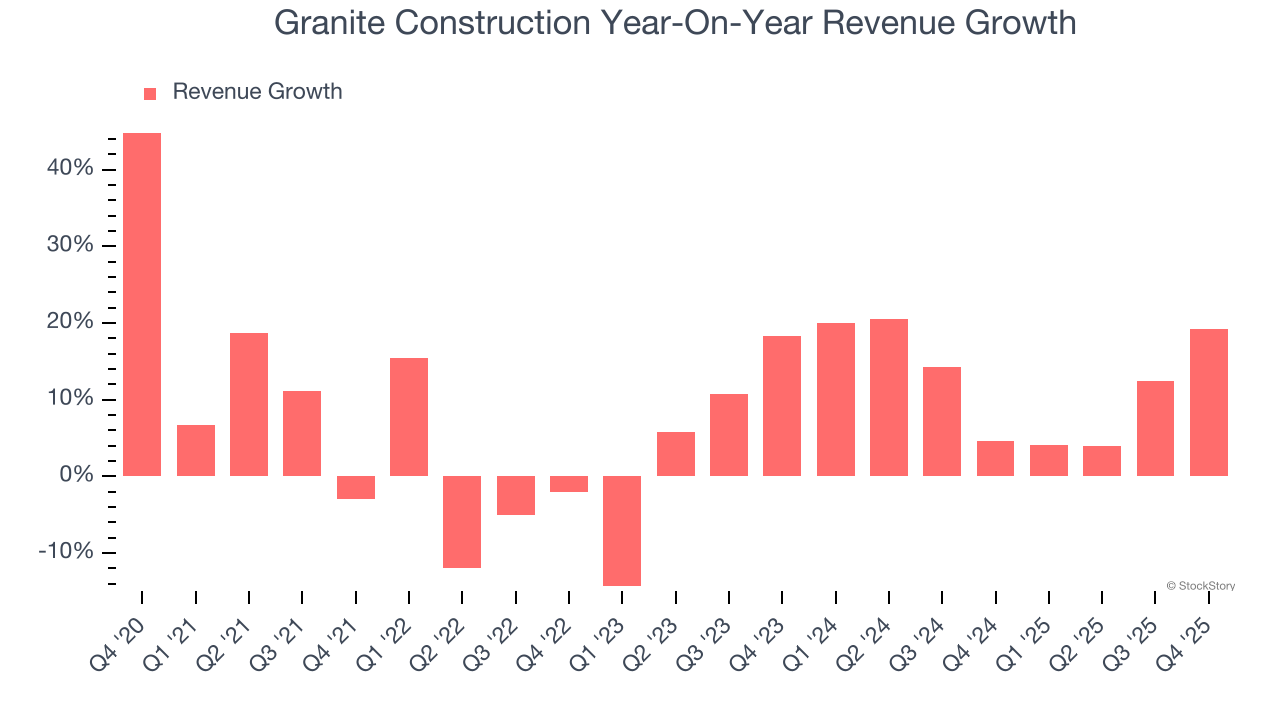

1. Skyrocketing Revenue Shows Strong Momentum

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Granite Construction’s annualized revenue growth of 12.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

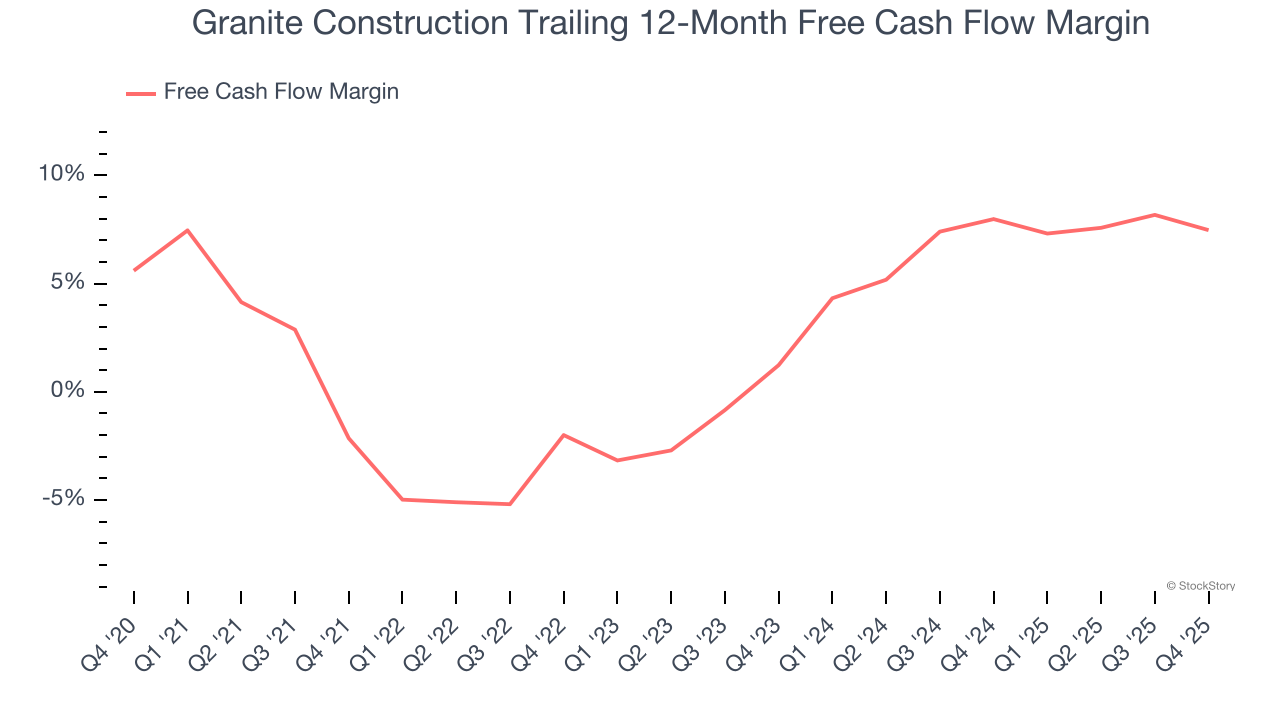

2. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Granite Construction’s margin expanded by 9.6 percentage points over the last five years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Granite Construction’s free cash flow margin for the trailing 12 months was 7.5%.

One Reason to be Careful:

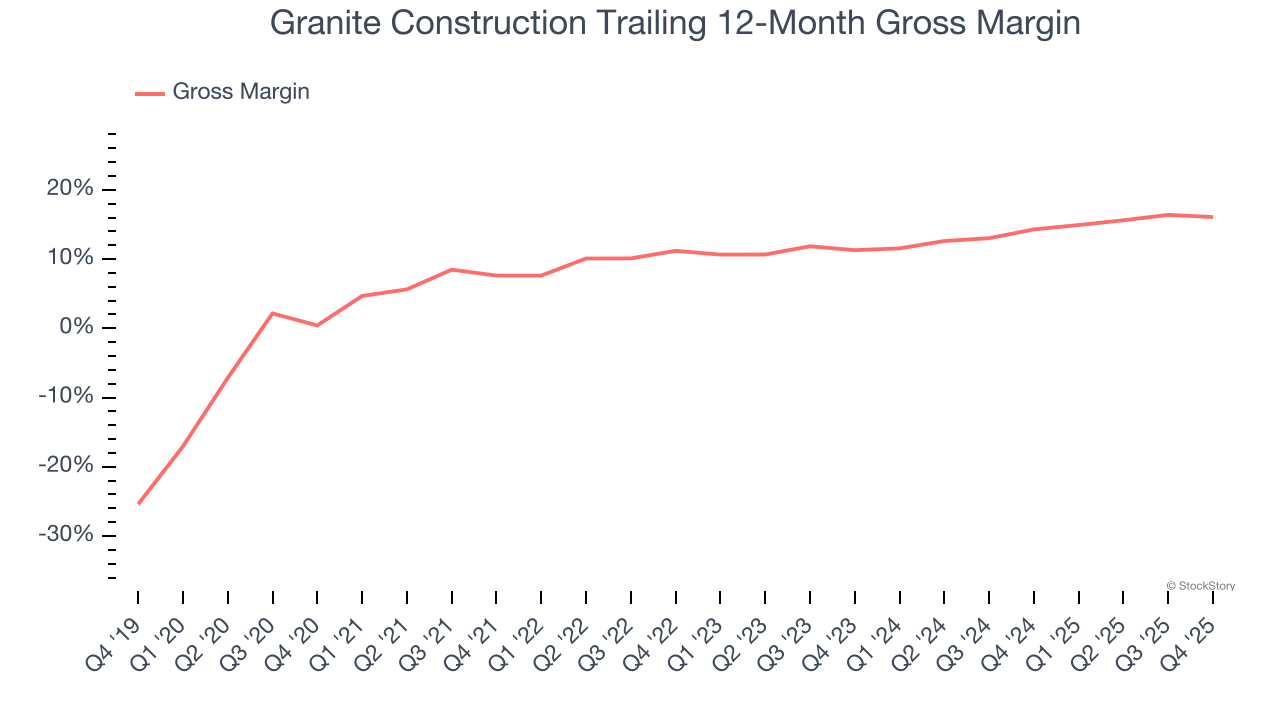

Low Gross Margin Reveals Weak Structural Profitability

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Granite Construction has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 12.4% gross margin over the last five years. That means Granite Construction paid its suppliers a lot of money ($87.61 for every $100 in revenue) to run its business.

Final Judgment

Granite Construction’s positive characteristics outweigh the negatives, and with its shares outperforming the market lately, the stock trades at 20× forward P/E (or $121.57 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Granite Construction

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.