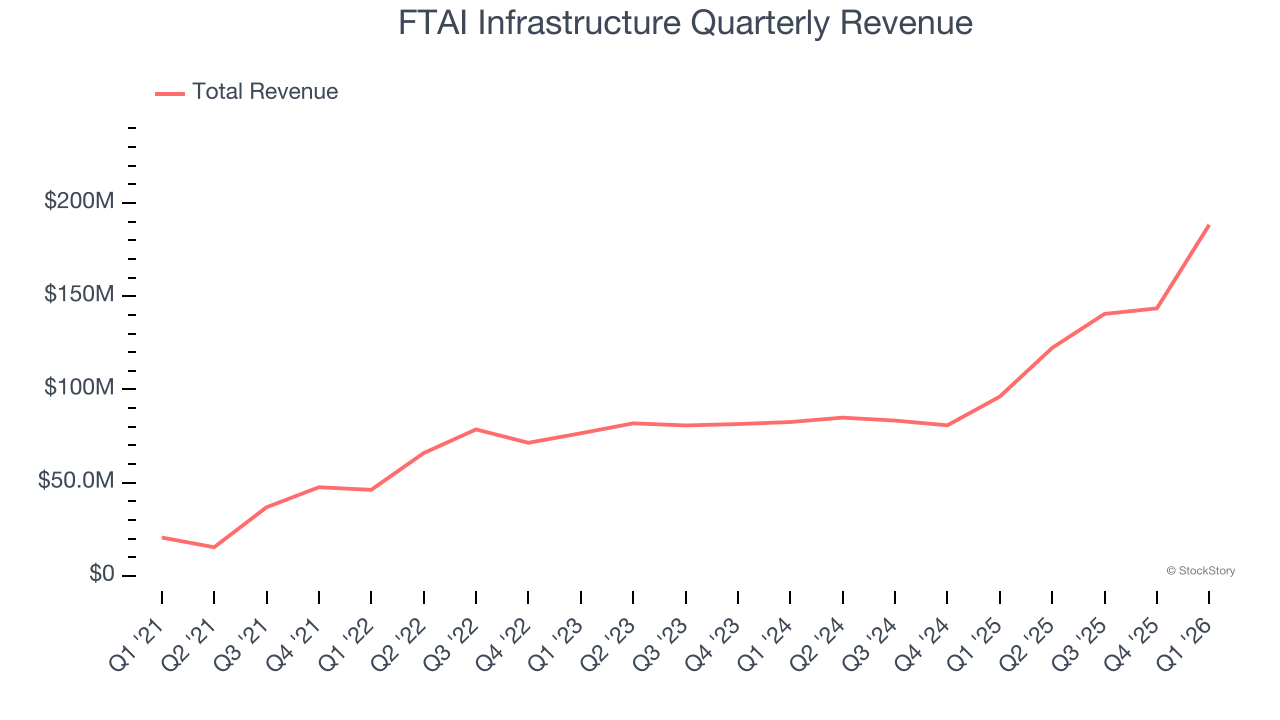

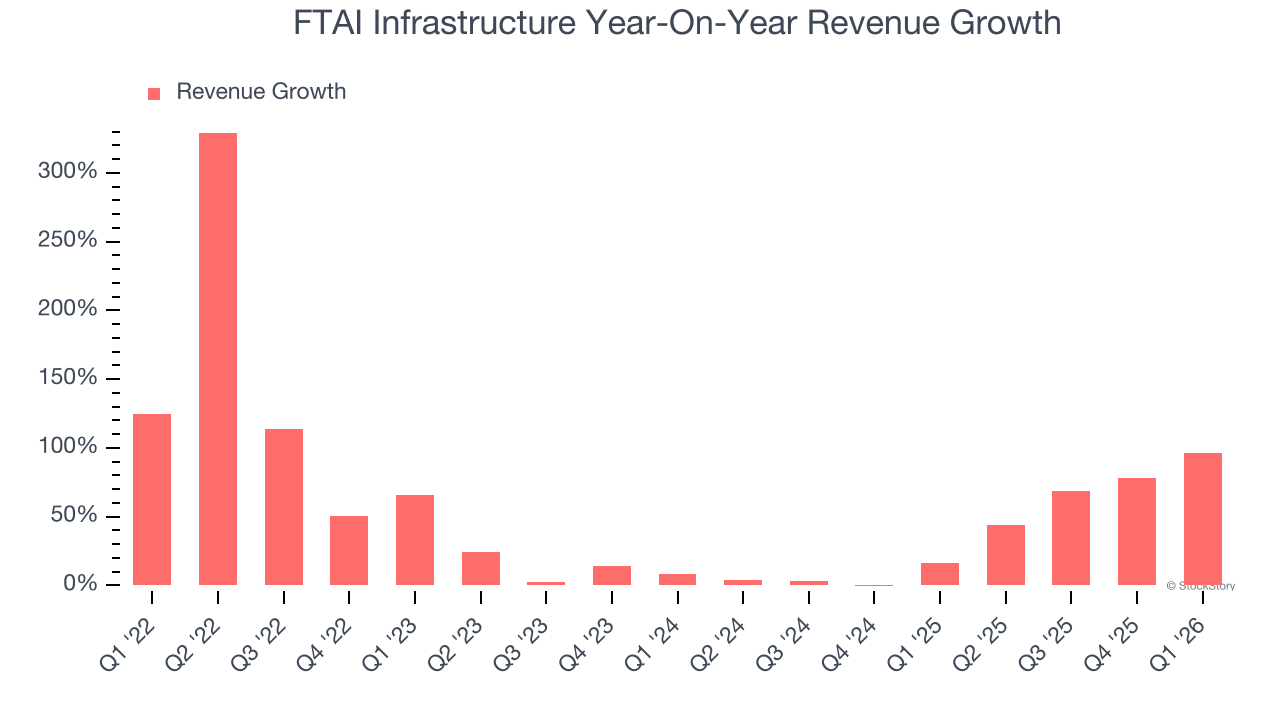

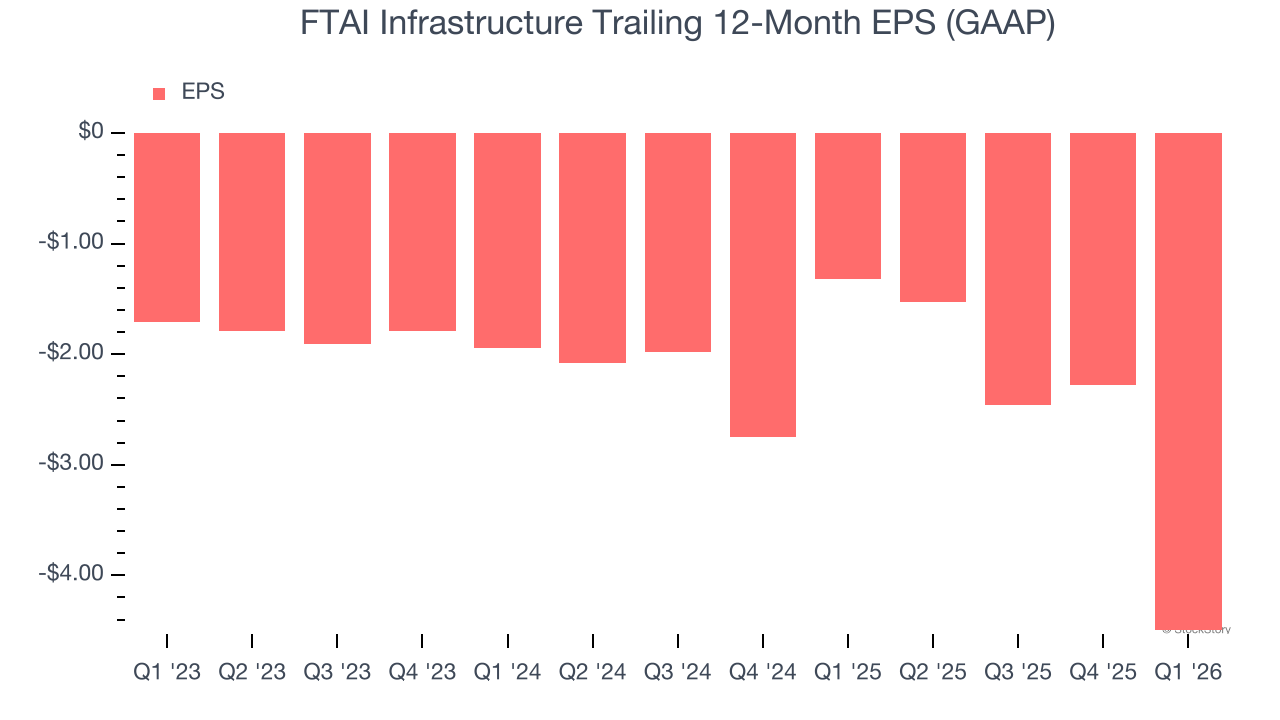

Infrastructure investment and operations firm FTAI Infrastructure (NASDAQ: FIP) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 95.9% year on year to $188.4 million. Its GAAP loss of $1.32 per share was significantly below analysts’ consensus estimates.

Is now the time to buy FTAI Infrastructure? Find out by accessing our full research report, it’s free.

FTAI Infrastructure (FIP) Q1 CY2026 Highlights:

- Revenue: $188.4 million vs analyst estimates of $182.4 million (95.9% year-on-year growth, 3.3% beat)

- EPS (GAAP): -$1.32 vs analyst estimates of -$0.42 (significant miss)

- Adjusted EBITDA: $70.59 million vs analyst estimates of $81.18 million (37.5% margin, 13% miss)

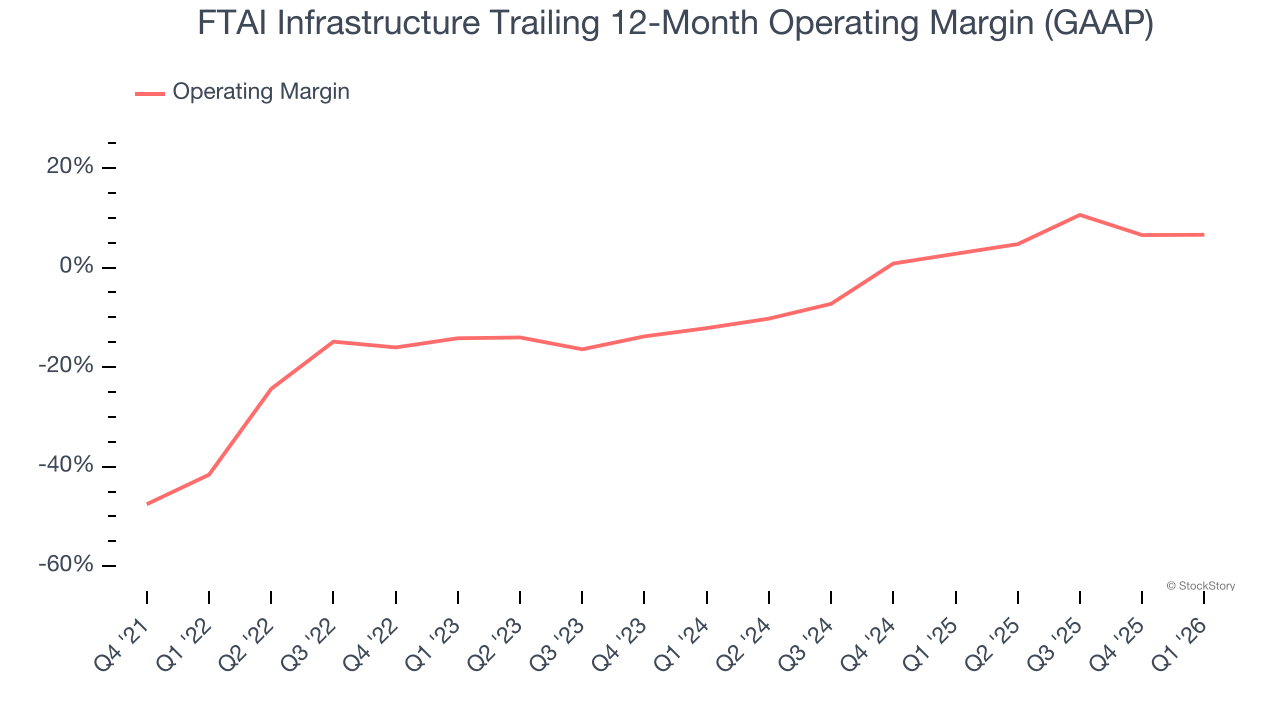

- Operating Margin: 1.5%, up from -3.7% in the same quarter last year

- Free Cash Flow was -$115.9 million compared to -$152.7 million in the same quarter last year

- Market Capitalization: $654.6 million

Company Overview

Spun off from FTAI Aviation in 2021, FTAI Infrastructure (NASDAQ: FIP) invests in and operates infrastructure and related assets across the transportation and energy sectors.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last four years, FTAI Infrastructure grew its sales at an incredible 42.1% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. FTAI Infrastructure’s annualized revenue growth of 35% over the last two years is below its four-year trend, but we still think the results suggest healthy demand.

This quarter, FTAI Infrastructure reported magnificent year-on-year revenue growth of 95.9%, and its $188.4 million of revenue beat Wall Street’s estimates by 3.3%.

Looking ahead, sell-side analysts expect revenue to grow 40.5% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Although FTAI Infrastructure was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 5.5% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, FTAI Infrastructure’s operating margin rose by 48.2 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

This quarter, FTAI Infrastructure generated an operating margin profit margin of 1.5%, up 5.2 percentage points year on year. The increase was driven by stronger leverage on its cost of sales (not higher efficiency with its operating expenses), as indicated by its larger rise in gross margin.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

FTAI Infrastructure’s earnings losses deepened over the last three years as its EPS dropped 42.4% annually. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For FTAI Infrastructure, its two-year annual EPS declines of 52.1% show it’s continued to underperform. These results were bad no matter how you slice the data, but given it was successful in other measures of financial health, we’re hopeful FTAI Infrastructure can generate earnings growth in the future.

In Q1, FTAI Infrastructure reported EPS of negative $1.32, down from $0.89 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects FTAI Infrastructure to improve its earnings losses. Analysts forecast its full-year EPS of negative $4.49 will advance to negative $1.16.

Key Takeaways from FTAI Infrastructure’s Q1 Results

We enjoyed seeing FTAI Infrastructure beat analysts’ revenue expectations this quarter. On the other hand, its adjusted operating income missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.7% to $4.99 immediately following the results.

FTAI Infrastructure may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).