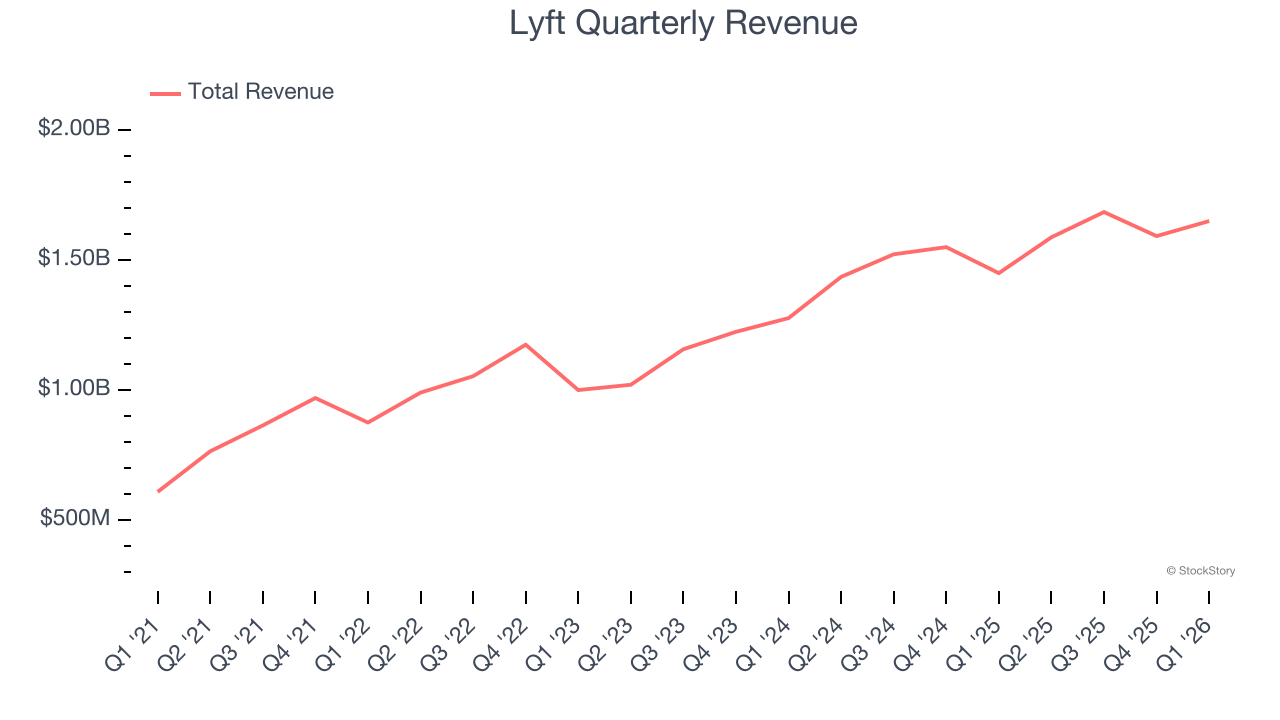

Ride sharing service Lyft (NASDAQ: LYFT) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 13.8% year on year to $1.65 billion. Its GAAP profit of $0.04 per share was 44.3% below analysts’ consensus estimates.

Is now the time to buy Lyft? Find out by accessing our full research report, it’s free.

Lyft (LYFT) Q1 CY2026 Highlights:

- Revenue: $1.65 billion vs analyst estimates of $1.63 billion (13.8% year-on-year growth, 1% beat)

- EPS (GAAP): $0.04 vs analyst expectations of $0.07 (44.3% miss)

- Adjusted EBITDA: $132.8 million vs analyst estimates of $130.7 million (8% margin, 1.6% beat)

- EBITDA guidance for Q2 CY2026 is $170 million at the midpoint, above analyst estimates of $167.3 million

- Operating Margin: -0.3%, up from -2% in the same quarter last year

- Free Cash Flow Margin: 17.4%, up from 14.3% in the previous quarter

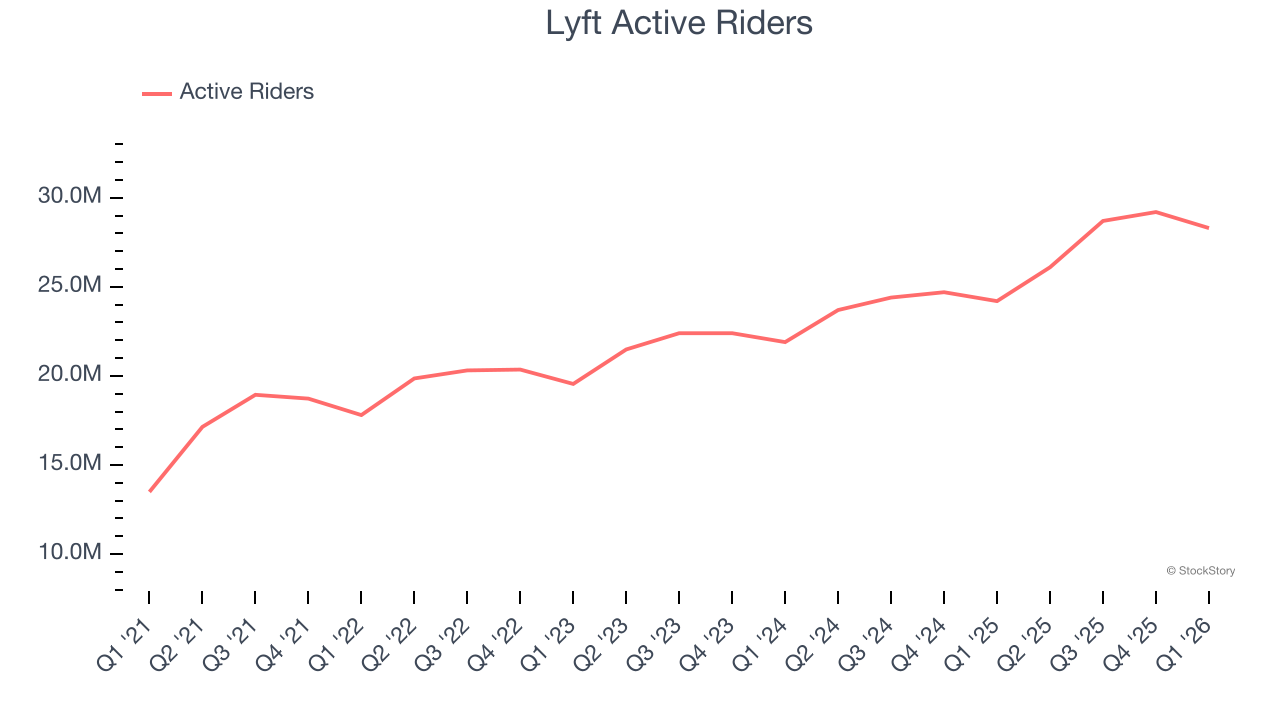

- Active Riders: 28.3 million, up 4.1 million year on year

- Market Capitalization: $5.44 billion

Company Overview

Founded by Logan Green and John Zimmer as a long-distance intercity carpooling company Zimride, Lyft (NASDAQ: LYFT) operates a ridesharing network in the US and Canada.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Lyft’s 15.6% annualized revenue growth over the last three years was solid. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Lyft reported year-on-year revenue growth of 13.8%, and its $1.65 billion of revenue exceeded Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 15.3% over the next 12 months, similar to its three-year rate. This projection is admirable and indicates the market is forecasting success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Active Riders

User Growth

As a gig economy marketplace, Lyft generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, Lyft’s active riders, a key performance metric for the company, increased by 12.9% annually to 28.3 million in the latest quarter. This growth rate is strong for a consumer internet business and indicates people love using its offerings.

In Q1, Lyft added 4.1 million active riders, leading to 16.9% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating user growth.

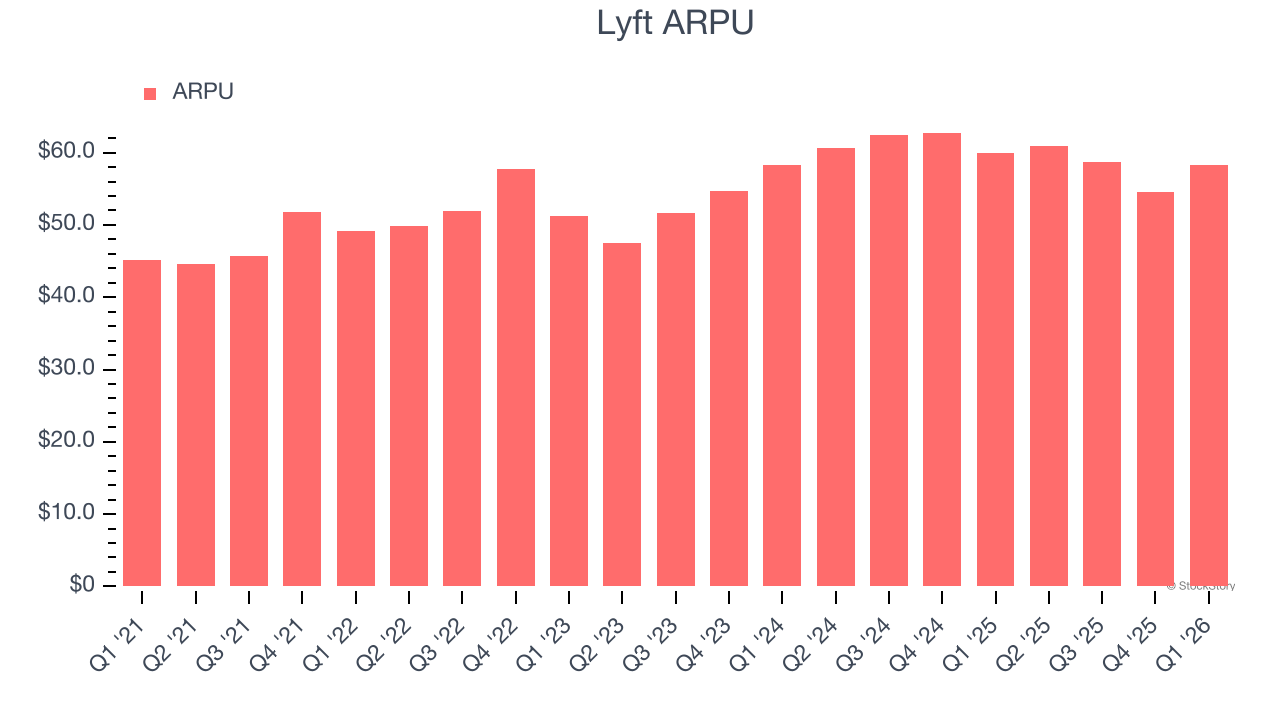

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. This number also informs us about Lyft’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Lyft’s ARPU growth has been decent over the last two years, averaging 5.6%. Its ability to increase monetization while effectively growing its active riders demonstrates the value of its platform.

This quarter, Lyft’s ARPU clocked in at $58.32. It declined 2.7% year on year, worse than the change in its active riders.

Key Takeaways from Lyft’s Q1 Results

It was great to see Lyft increase its number of users this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 3.1% to $13.72 immediately after reporting.

Is Lyft an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).