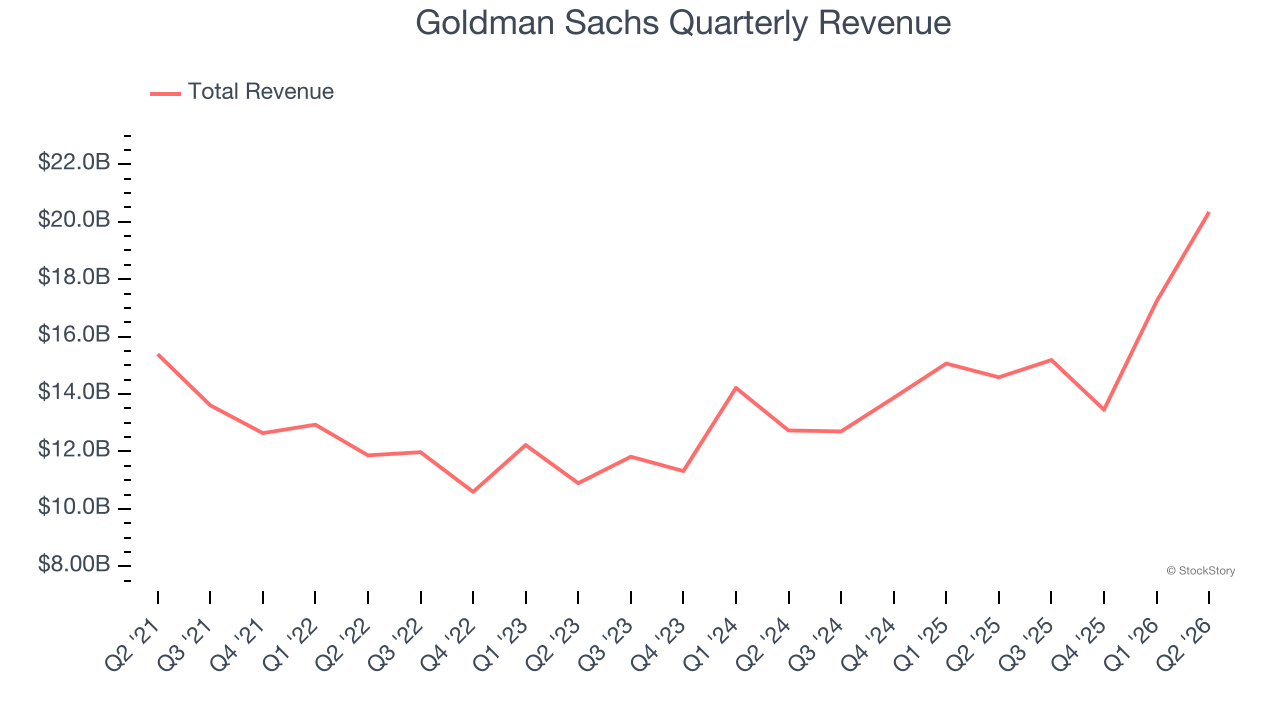

Global investment bank Goldman Sachs (NYSE: GS) beat Wall Street’s revenue expectations in Q2 CY2026, with sales up 39.5% year on year to $20.34 billion. Its GAAP profit of $20.98 per share was 44.3% above analysts’ consensus estimates.

Is now the time to buy Goldman Sachs? Find out by accessing our full research report, it’s free.

Goldman Sachs (GS) Q2 CY2026 Highlights:

- Revenue: $20.34 billion vs analyst estimates of $16.44 billion (39.5% year-on-year growth, 23.7% beat)

- Pre-tax Profit: $8.56 billion (42.1% margin)

- EPS (GAAP): $20.98 vs analyst estimates of $14.54 (44.3% beat)

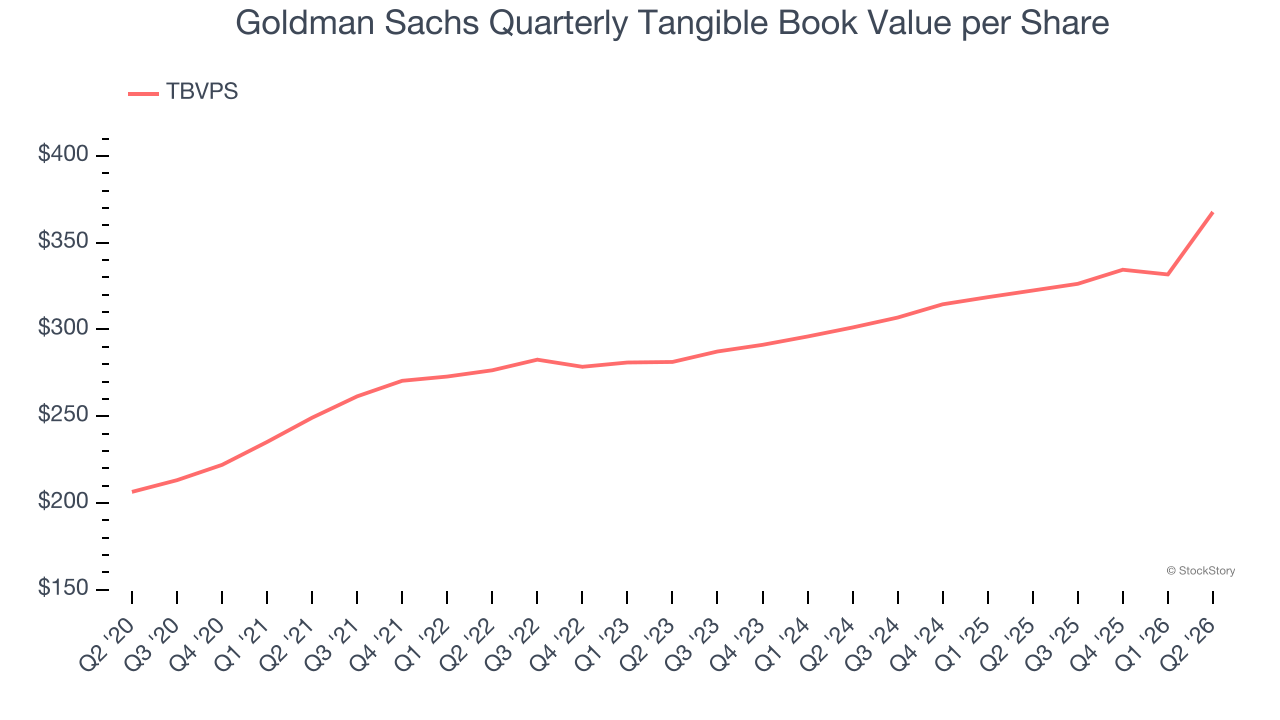

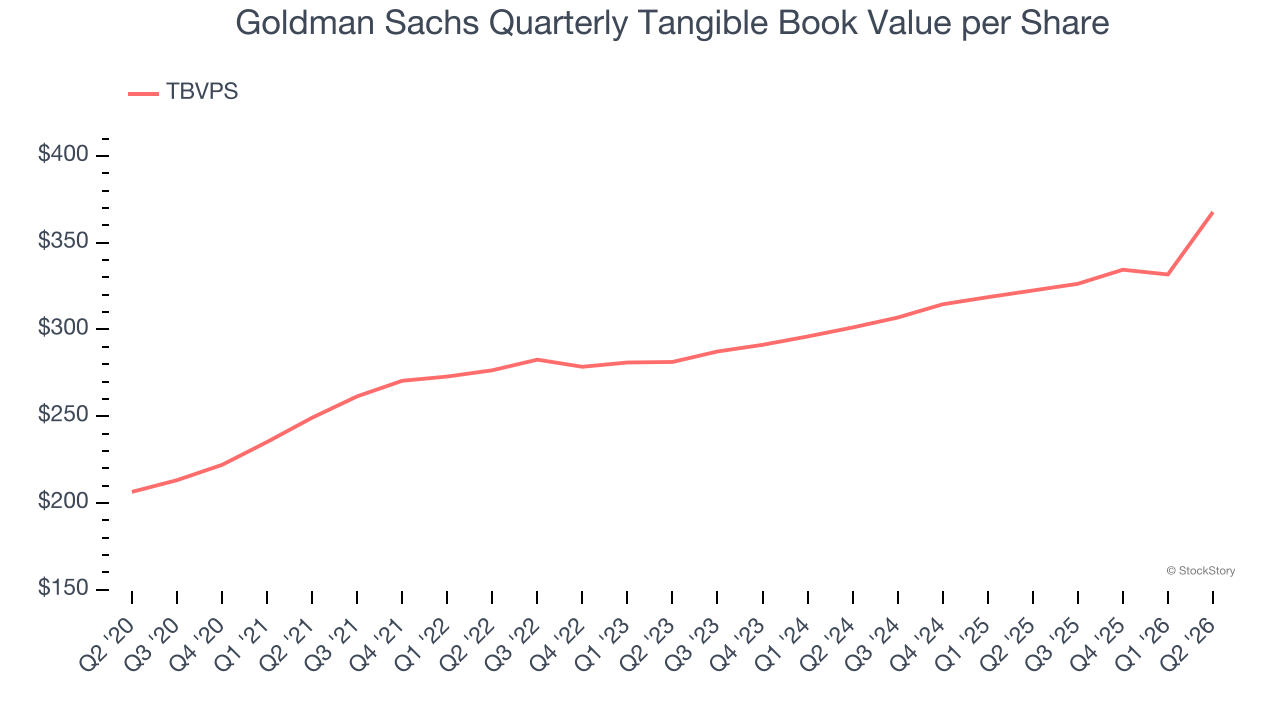

- Tangible Book Value per Share: $367.67 vs analyst estimates of $341.83 (14% year-on-year growth, 7.6% beat)

- Market Capitalization: $320.7 billion

Company Overview

Founded in 1869 as a small commercial paper business in New York City, Goldman Sachs (NYSE: GS) is a global financial institution that provides investment banking, securities, asset management, and consumer banking services to corporations, governments, and individuals.

Revenue Growth

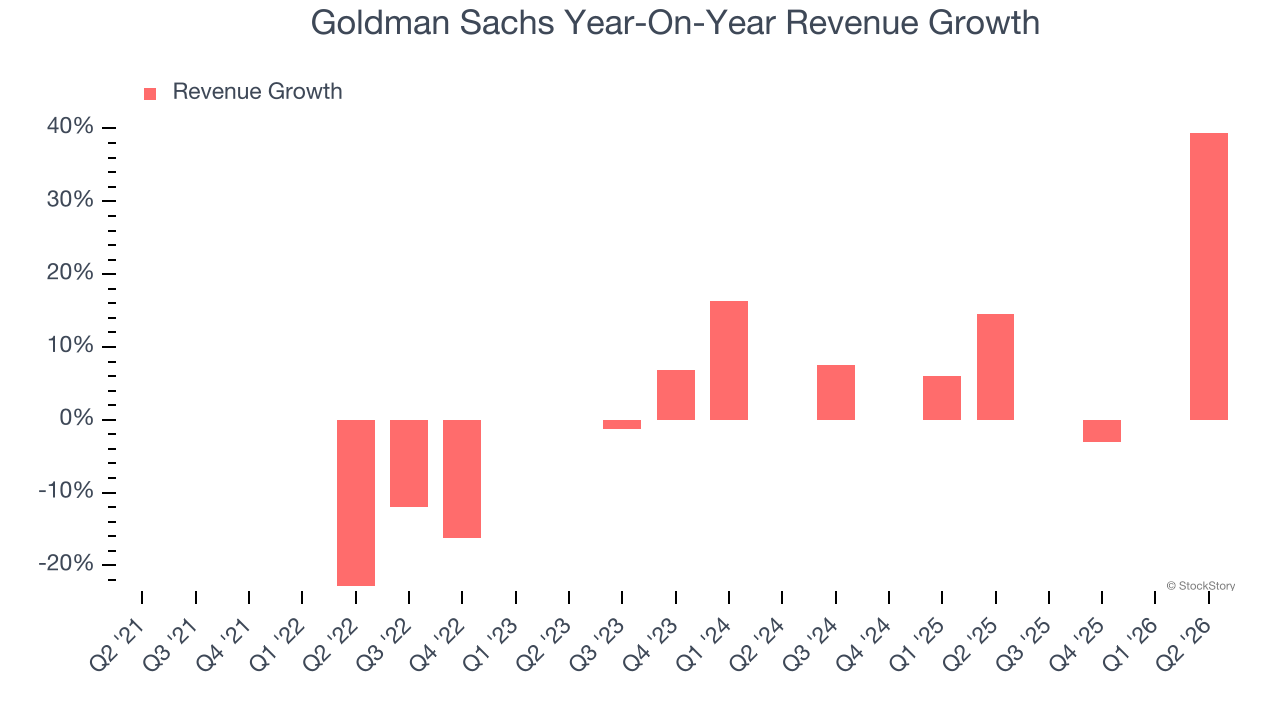

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Goldman Sachs’s 3.5% annualized revenue growth over the last five years was sluggish. This was below our standard for the financials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Goldman Sachs’s annualized revenue growth of 15% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers because they were impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers because they were impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Goldman Sachs reported wonderful year-on-year revenue growth of 39.5%, and its $20.34 billion of revenue exceeded Wall Street’s estimates by 23.7%.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Tangible Book Value Per Share (TBVPS)

Financial institutions with multiple business lines manage complex balance sheets that span various financial activities. Market valuations reflect this operational complexity, prioritizing balance sheet strength and sustainable book value growth across all business segments.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark for the sector. This metric captures real, liquid net worth per share that reflects the institution’s overall financial health across all business lines. On the other hand, EPS is often distorted by the diverse nature of operations, mergers, and various accounting treatments across different business units. Book value provides clearer performance insights.

Goldman Sachs’s TBVPS grew at a decent 8.1% annual clip over the last five years. TBVPS growth has accelerated recently, growing by 10.5% annually over the last two years from $301.16 to $367.67 per share.

Tangible Book Value Per Share (TBVPS)

The balance sheet drives profitability for financial firms since earnings flow from managing diverse assets and liabilities across multiple business lines. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential across their varied operations.

When analyzing this sector, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value and provides insight into the institution’s capital position across diverse operations. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to the complexity of multiple business lines, M&A activity, or accounting rules that vary across different financial services segments.

Goldman Sachs’s TBVPS grew at a decent 8.1% annual clip over the last five years. TBVPS growth has accelerated recently, growing by 10.5% annually over the last two years from $301.16 to $367.67 per share.

Key Takeaways from Goldman Sachs’s Q2 Results

It was good to see Goldman Sachs beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.1% to $1,057 immediately after reporting.

Goldman Sachs had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).