The past six months have been a windfall for Moderna’s shareholders. The company’s stock price has jumped 46.4%, hitting $62.97 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Moderna, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Moderna Will Underperform?

Despite the momentum, we’re sitting this one out for now. Here are three reasons we avoid MRNA, plus one stock we’d rather own.

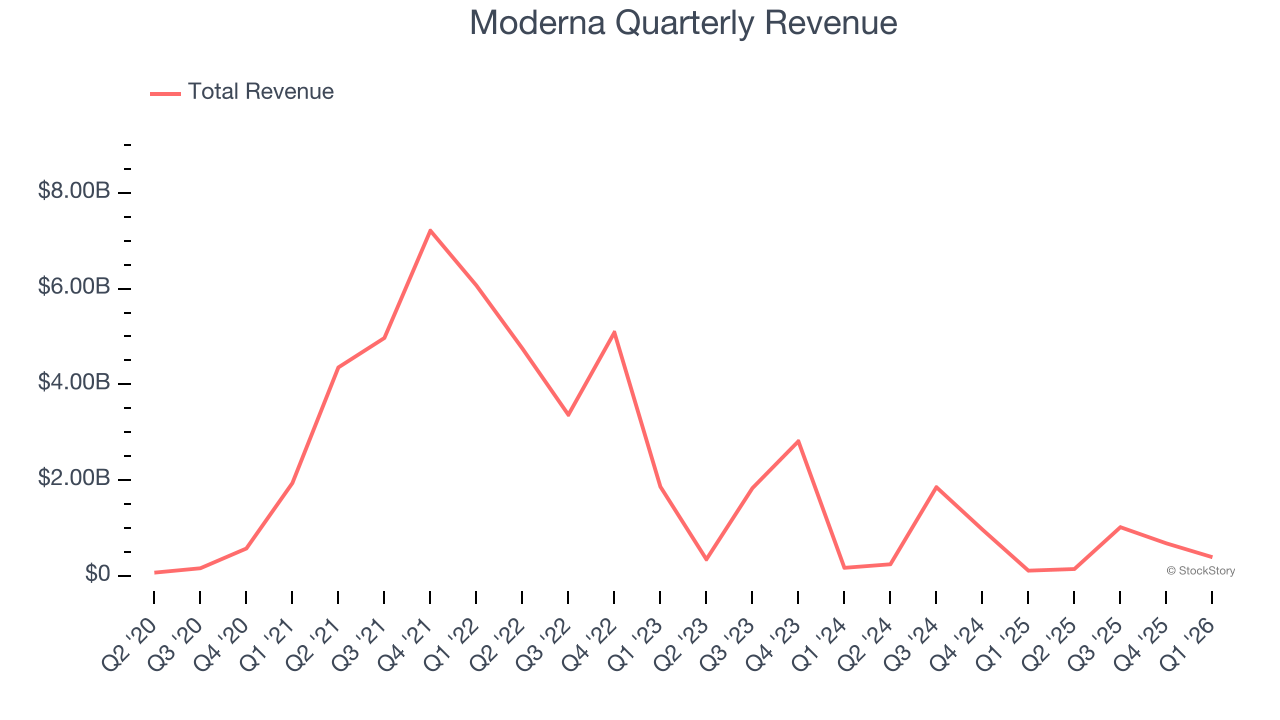

1. Revenue Spiraling Downwards

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Moderna’s demand was weak over the last five years as its sales fell at a 4% annual rate. This wasn’t a great result and signals it’s a low quality business.

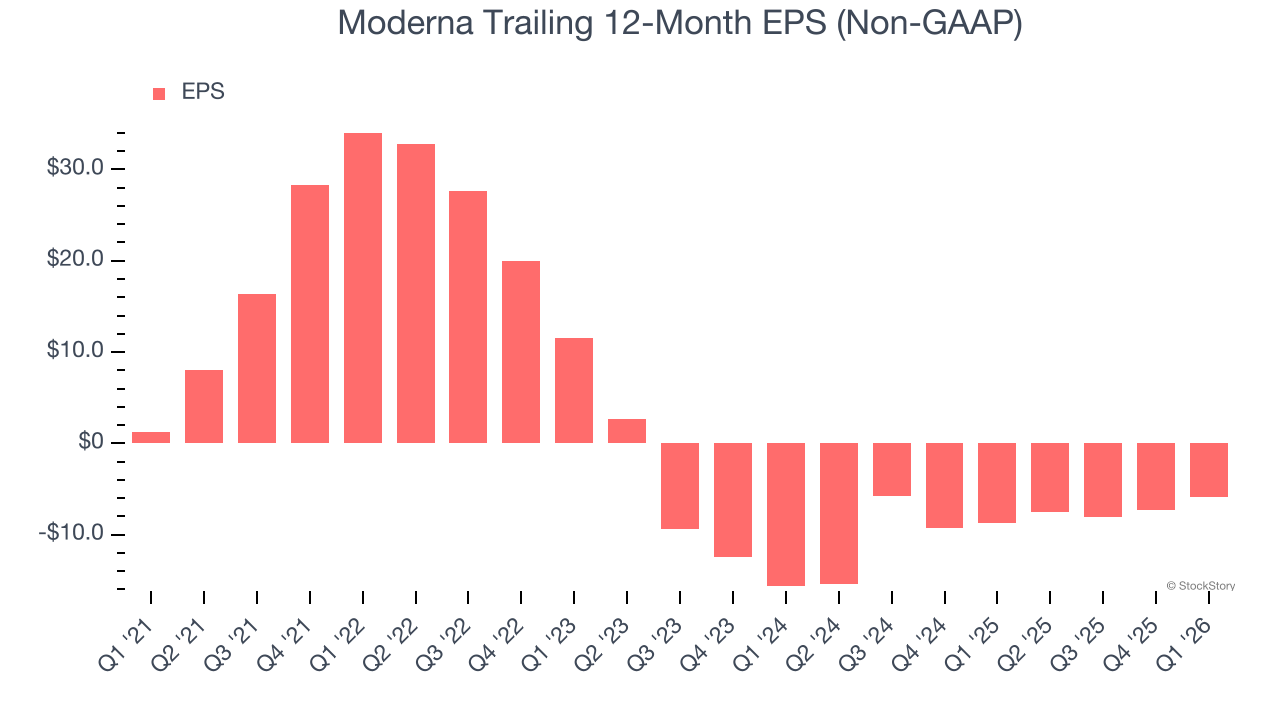

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Moderna, its EPS declined by 46.5% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

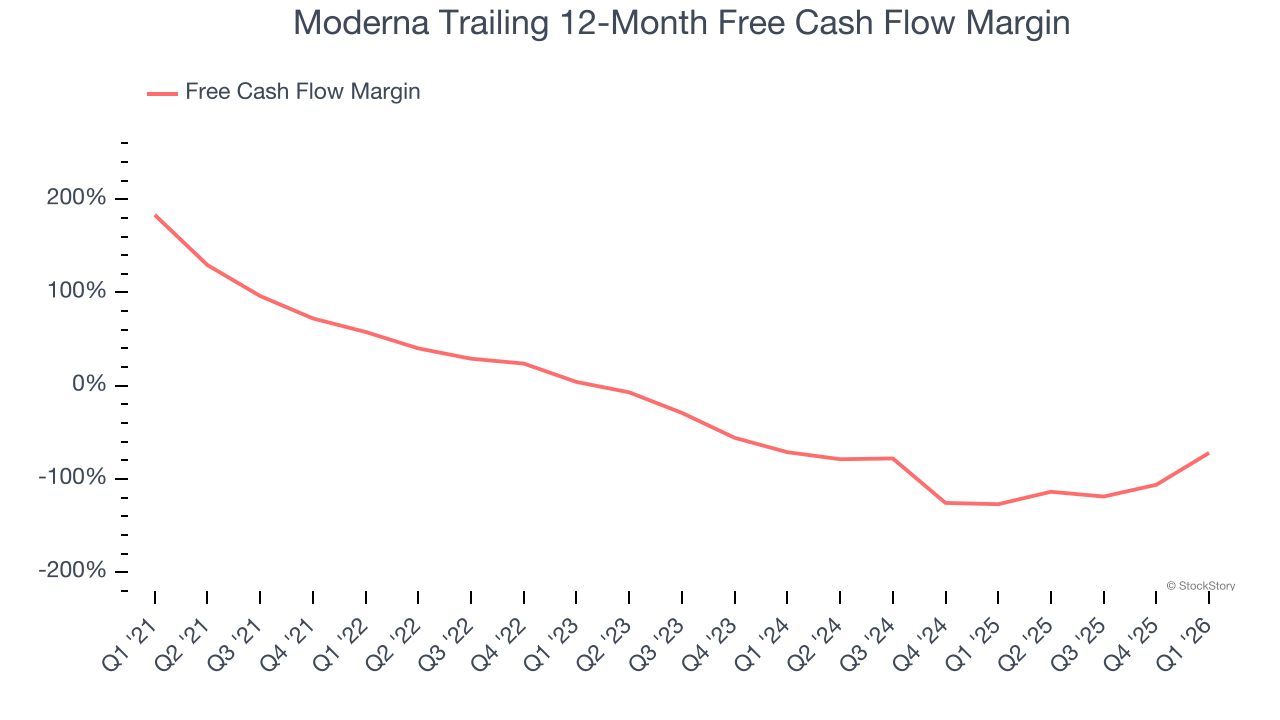

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Moderna’s margin dropped meaningfully over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal it is in the middle of an investment cycle. Moderna’s free cash flow margin for the trailing 12 months was negative 72%.

Final Judgment

Moderna doesn’t pass our quality test. Following the recent surge, the stock trades at $62.97 per share (or a forward price-to-sales ratio of 14×). The market typically values companies like Moderna based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. We’d recommend looking at one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662% between October 2022 and February 2026. AppLovin before it ran 753% between February 2024 and February 2026. Nvidia before it ran 1,178% between January 2023 and February 2026. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+1,154% between June 2020 and June 2025). Find your next big winner with StockStory today.