Diamondback Energy’s 27% return over the past six months has outpaced the S&P 500 by 19.2%, and its stock price has climbed to $187.18 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is it too late to buy FANG? Find out in our full research report, it’s free.

Why Are We Positive on Diamondback Energy?

Sporting one of Wall Street's most memorable ticker symbols, Diamondback Energy (NASDAQ: FANG) drills for and produces oil and natural gas from underground rock formations in the Permian Basin of West Texas and New Mexico.

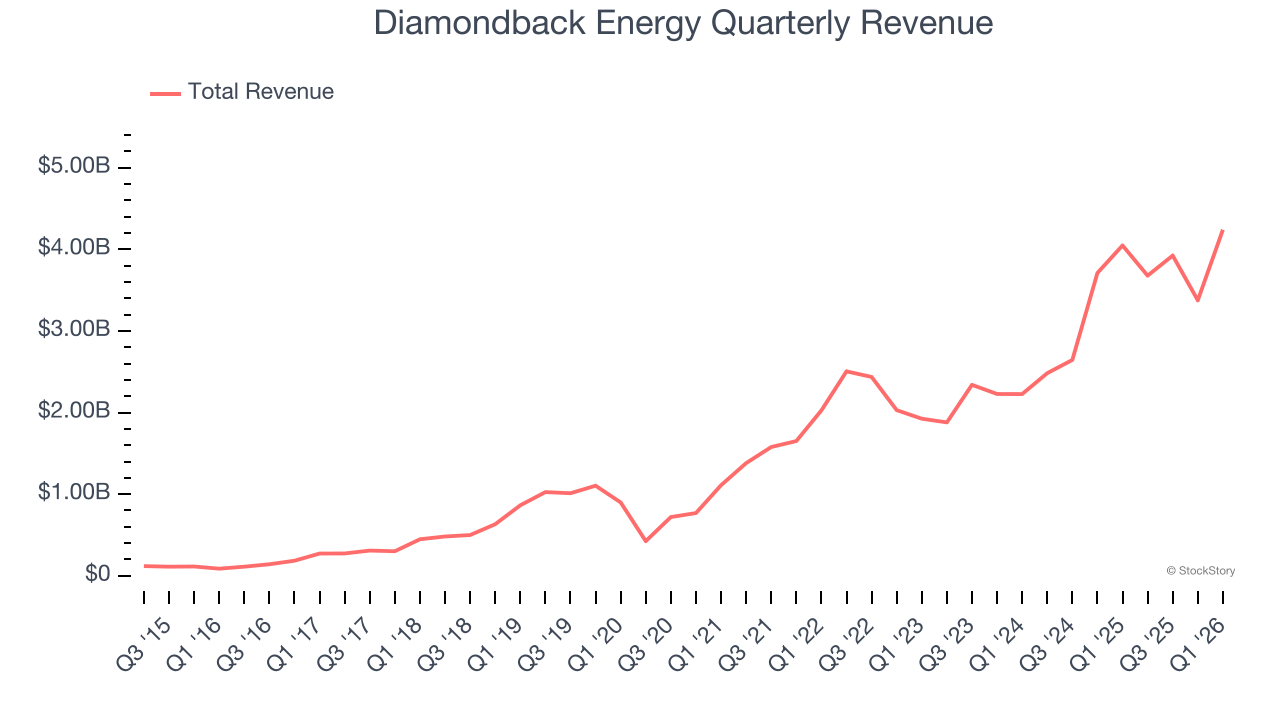

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Thankfully, Diamondback Energy’s 38.2% annualized revenue growth over the last five years was incredible. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

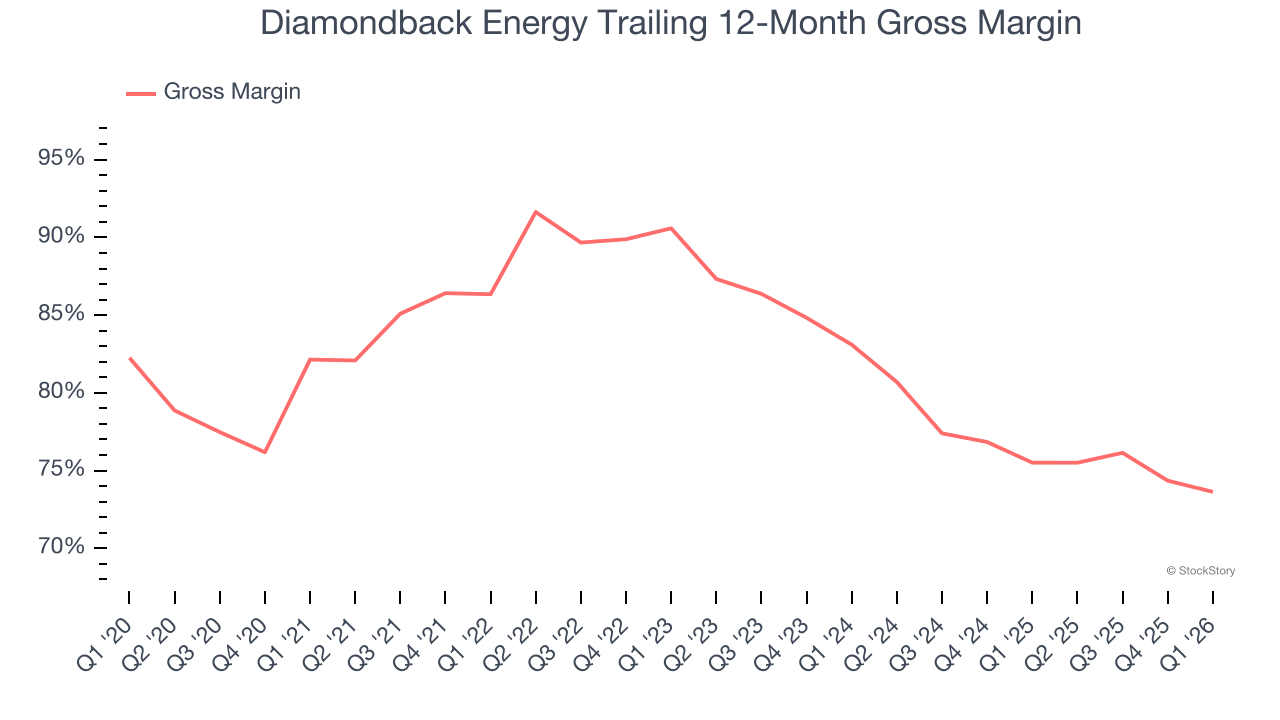

2. Elite Gross Margin Powers Best-In-Class Business Model

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

Diamondback Energy, which averaged 80.2% gross margin over the last five years, exhibits enviable unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an advantaged starting point for ultimate operating profits and free cash flow generation.

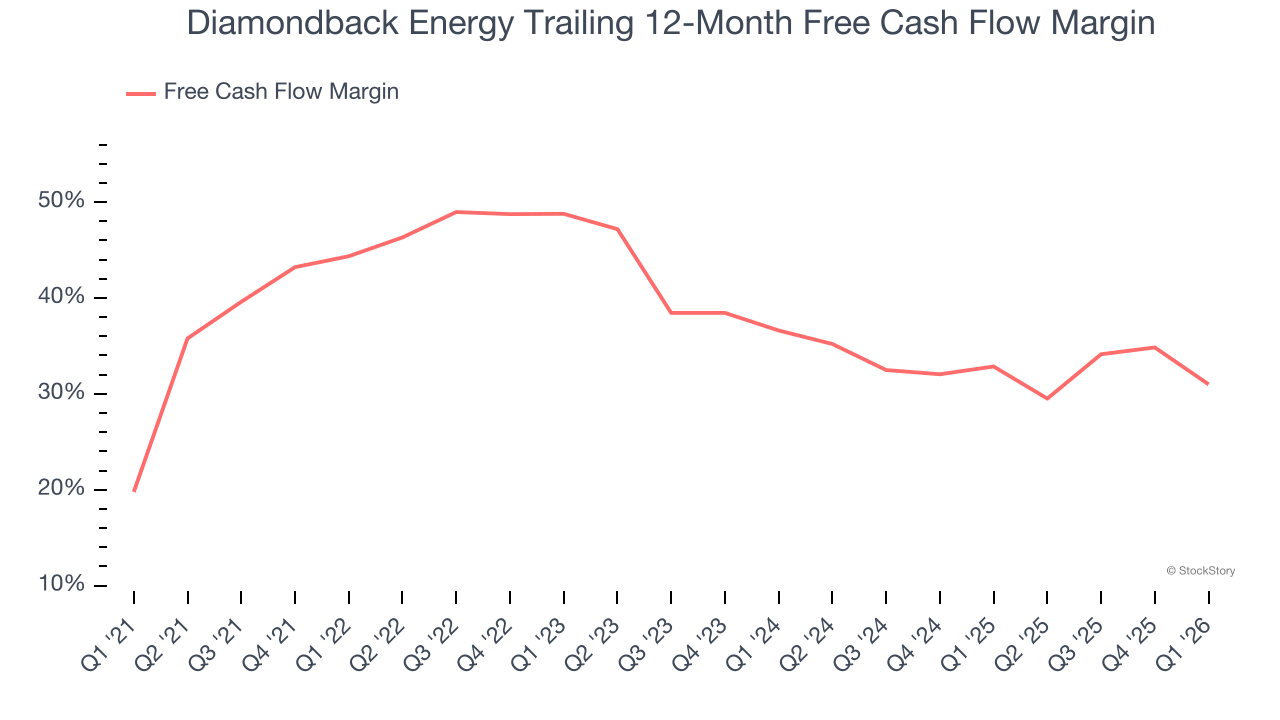

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Diamondback Energy has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging an eye-popping 37.1% over the last five years.

Final Judgment

These are just a few reasons why Diamondback Energy is a cream-of-the-crop energy upstream and integrated energy company, and with its shares topping the market in recent months, the stock trades at 8.6× forward P/E (or $187.18 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Diamondback Energy

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.