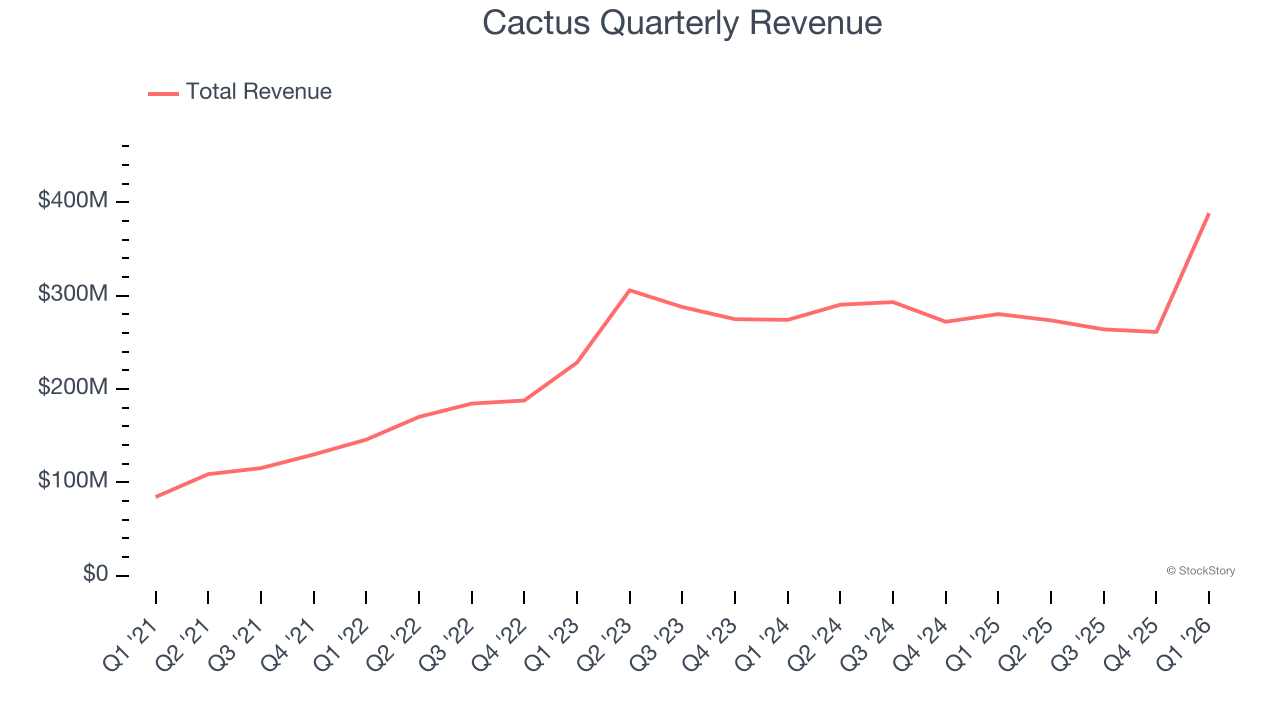

Oilfield equipment manufacturer Cactus (NYSE: WHD) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 38.5% year on year to $388.3 million. Its non-GAAP profit of $0.70 per share was 4.6% above analysts’ consensus estimates.

Is now the time to buy Cactus? Find out by accessing our full research report, it’s free.

Cactus (WHD) Q1 CY2026 Highlights:

- Revenue: $388.3 million vs analyst estimates of $379.7 million (38.5% year-on-year growth, 2.3% beat)

- Adjusted EPS: $0.70 vs analyst estimates of $0.67 (4.6% beat)

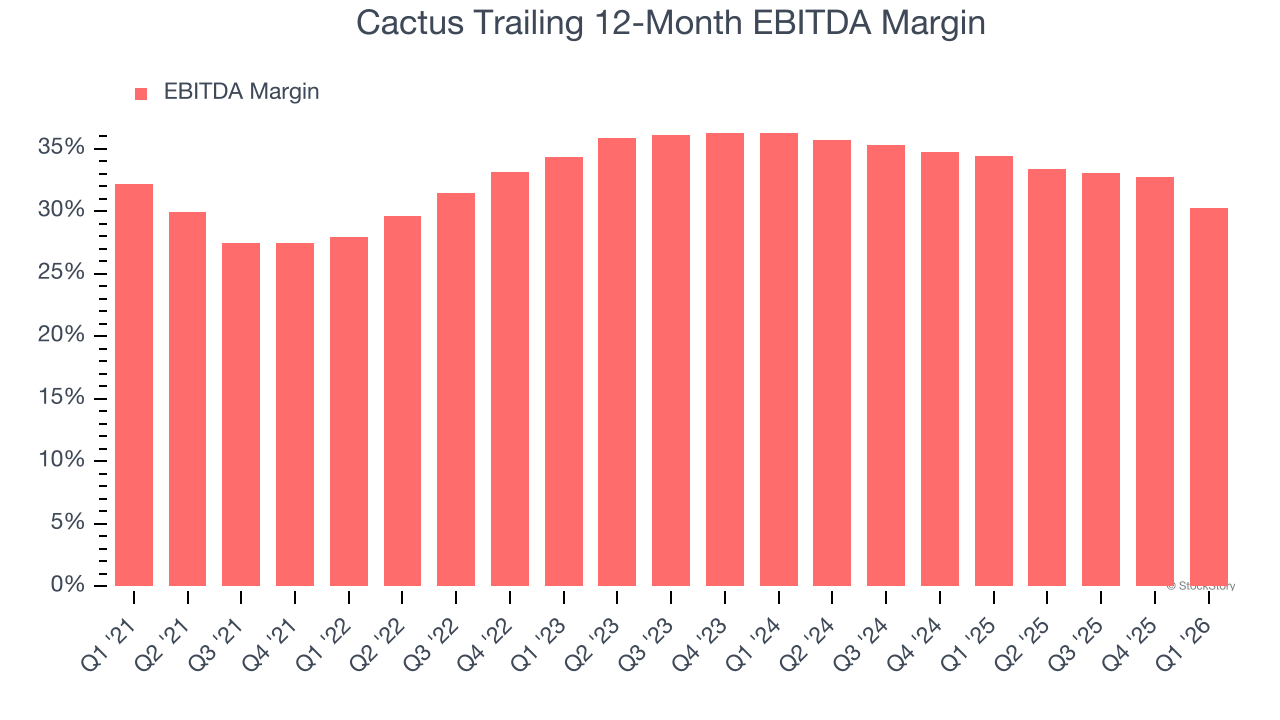

- Adjusted EBITDA: $100.1 million vs analyst estimates of $93.35 million (25.8% margin, 7.2% beat)

- Operating Margin: 12.7%, down from 24.5% in the same quarter last year

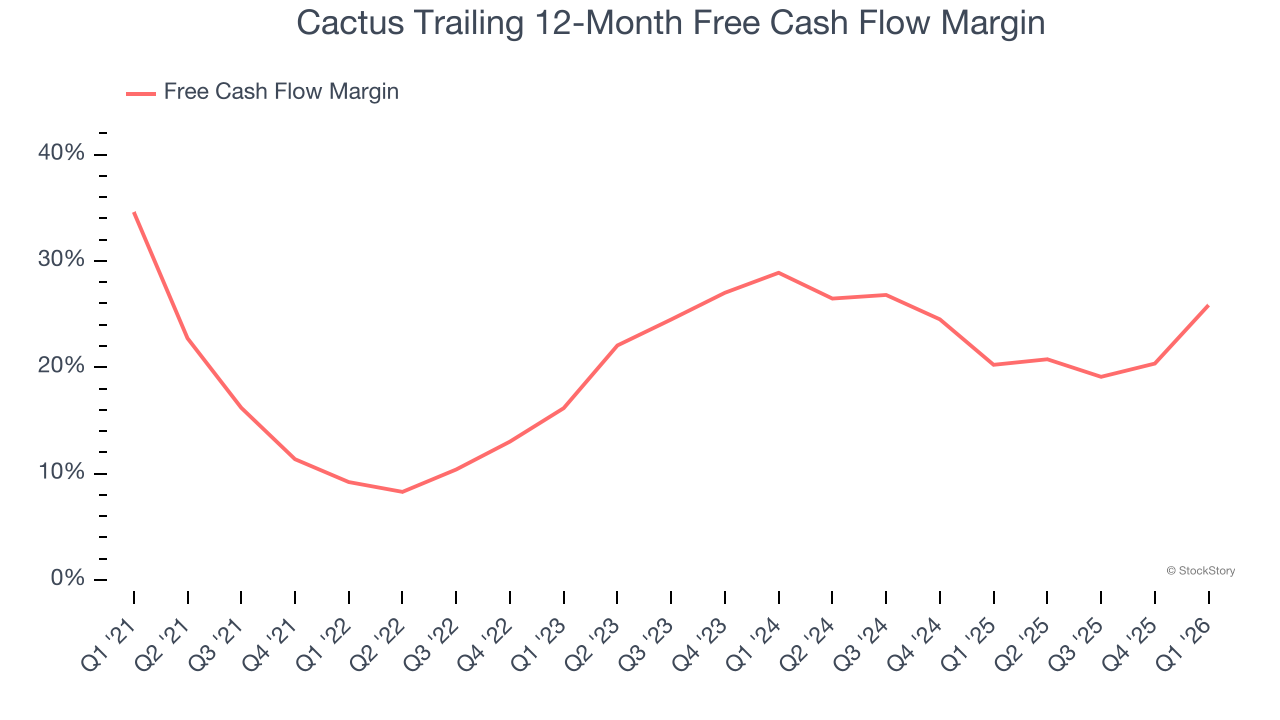

- Free Cash Flow Margin: 30.5%, up from 11.2% in the same quarter last year

- Market Capitalization: $3.78 billion

Company Overview

Named for the spiky wellhead equipment that reminded founders of desert cacti, Cactus (NYSE: WHD) manufactures wellheads, valves, and spoolable pipes used in drilling and producing oil and gas wells.

Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Thankfully, Cactus’s 33.6% annualized revenue growth over the last five years was incredible. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers, a great starting point for our analysis.

Energy cycles can be long enough that a single five-year period can still reflect one price environment, which is why an additional, decade-long view can help capture through-cycle performance. Cactus’s annualized revenue growth of 23.2% over the last nine years is below its five-year trend, but we still think the results suggest decent demand.

This quarter, Cactus reported wonderful year-on-year revenue growth of 38.5%, and its $388.3 million of revenue exceeded Wall Street’s estimates by 2.3%.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted EBITDA Margin

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Cactus has done a decent job managing its cost base over the last five years. The company has produced an average EBITDA margin of 33.1%, higher than the broader energy upstream and integrated energy sector.

Looking at the trend in its profitability, Cactus’s EBITDA margin rose by 2.3 percentage points over the last year, as its sales growth gave it operating leverage.

In Q1, Cactus generated an EBITDA margin profit margin of 25.8%, down 7.7 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue. This adjusted EBITDA beat Wall Street’s estimates by 7.2%.

Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Cactus has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging 21.9% over the last five years.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

Cactus’s ratio of quarterly free cash flow volatility to WTI Crude price volatility over the past five years was 4.1 (lower is better), indicating unusually strong insulation from commodity swings. This stability supports superior capital access in downturns and positions Cactus to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of Cactus? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Cactus’s free cash flow clocked in at $118.5 million in Q1, equivalent to a 30.5% margin. This result was good as its margin was 19.4 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from Cactus’s Q1 Results

We enjoyed seeing Cactus beat analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 2.3% to $55.75 immediately following the results.

Cactus had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).